What Is Wrong With Health Care, Though My Diagnosis is Opposite of the Left's

Note: I did not like the way I first wrote this post so I have re-written it extensively.

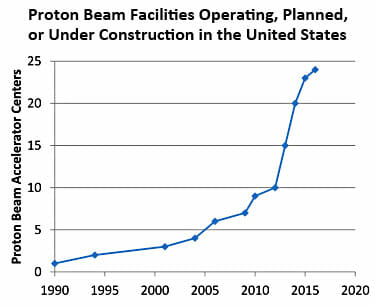

Progressives are passing around this chart from Brookings as an indicator of "what is wrong" with the US healthcare system.

This is how Kevin Drum interprets the chart:

In other words, the supposed advantage of PRT—that it targets cancers more precisely and has fewer toxic side effects—doesn't seem to be true. It might be better in certain very specialized cases, but not for garden variety prostate cancer.

And yet, new facilities are being constructed at a breakneck pace. Why? Because if they build them, patients will come. "They're simply done to generate profits," says health care advisor Ezekiel Emanuel. Roger that.

This is an analysis that may be true, but let's take a moment to consider how strange it is. Forget health care for a minute. Think about any other industry. Here is what they are effectively saying:

- Industry competitors are making huge investments in a technology that has no consumer value

- The competitors in this industry are all making investments in this technology so rapidly that the industry is exponentially over-saturating with capacity.

And from these two facts they conclude that the profits of industry competitors will increase??

Let's for a moment say this is true -- an enormous investment that has no customer utility and that is made by so many players that the market is quickly over-saturated actually increases industry profits. Let's take a moment to recognize that this is BIZARRE. We have to be suspicious of some structural issue for something so bizarre to happen. As is typical of progressives, their diagnosis seems to be that private actors are somehow at fault for being bad people to make these investments. But these same private actors, even if they wanted to, could never make this work in any other industry, and besides there is no evidence that hospital managers are any worse people than, say, cookie company managers. The problem is that we have fashioned a bizarre system through heavy government intervention that apparently makes these pointless investments sensible to otherwise rational actors.

One problem is that in any normal industry, consumers would simply refuse to buy, or at least refuse to pay a very high price, for services that have little or no value. But in health care, we have completely eliminated any consumer visibility to prices. Worse, we have eliminated any incentive for them to care about prices or really even the utility of a given procedure. This proton beam thingie might improve my outcomes 1%? Why not, it's not costing me anything. Perhaps the biggest problem in health care is that the consumer has no incentive to shop. Obamacare does nothing to fix this issue, and in fact if anything is taking us further away from consumer shopping and price transparency by working to kill high deductible health insurance and HSA's.

There is only one other industry I can think of where capital investment, even stupid capital investment, automatically translates to more profits, and that is the regulated utility business. And that is what hospitals have become -- regulated utilities that get nearly automatic returns on investment.

In a truly free market, if these investments made no sense, one would expect very soon a reckoning as those who made these nutty investments go bankrupt. But they obviously don't expect this. They expect that even if it turns out to be a bad investment, they will use their political ties to get these costs built into their rate base (essentially built into reimbursement rates). If any private or public entity refuses to pay, you just run around screaming to the media that they want to deny old people care and let sick people die. Further, the government can't let large hospitals go bankrupt because it has already artificially limited their supply through certificate of need processes in most parts of the country.

The Left has proposed to fix this by creating the IPAB, a group so divorced from accountability that it can theoretically make unpopular care rationing decisions and survive the political fallout. But the cost of this approach is enormous, as it essentially creates an un-elected dictatorship for 1/7 of the economy. Which tends to be awesome if your interests and preferences line up with those of the dictator, but sucks for everyone else. Which category do you expect to be in? (Oh, and let's not forget how many examples we have from history of benevolent technocratic dictatorships - zero.)

The much more reasonable solution, of course, is to handle these issues the same way we do in cookies and virtually every other product -- let consumers make price-value tradeoffs with their own money.