President Trump said he will ban large investors from buying single-family homes, the administration’s first significant move to address the country’s severe housing shortage.

“I am immediately taking steps to ban large institutional investors from buying more single-family homes, and I will be calling on Congress to codify it. People live in homes, not corporations,” Trump said in a social-media post Wednesday.

I tell folks all the time that Trump is not a freaking free-marketeer. This is yet more evidence. His proposal is right out of the failed Progressive-Socialist playbook on housing. Some quick thoughts:

Except where the houses have been converted to overnight rentals (think Airbnb or VRBO), people still live in these institutionally owned houses. This is not withdrawing housing stock from the market, it is merely shifting it from individual purchase to rentals. And there are arguments for there being more not less rental houses -- particularly when interest rates are high and/or housing prices are flat, houses limit mobility by locking a family to a fixed position, limiting the ability to seek out better employment in other cities

There is something to be said for renting from an institution, rather than an individual owner, as these landlords have better systems, large support and maintenance staffs, and often better legal compliance. Because living in certain neighborhood boundaries is required to attend the best public schools, this allows families who could not afford to buy a house in that neighborhood to be able to live there. It also opens suburban living to young couples who have not yet saved a down payment.

According to the WSJ, these institutions own 2-3% of the housing stock at most. Hard to imagine that this tail is wagging the dog. This is a typical populist grandstanding proposal with zero ability to address the intended issue, but a lot of emotional resonance with swing voters.

Real housing prices were likely flat to slightly down in 2025, so if there is a current "affordability" crisis it has more to do with higher mortgage rates than housing prices per se. Rents have increased faster than inflation the last several years, but its hard to figure how removing rental units from the market based on this order will do anything to lower rents.

No one was complaining about institutional buyers back in 2008 when the market was awash in unsold houses and institutions began soaking up this excess capacity and providing much needed liquidity to the market.

I will confess the endless calls and texts to my cell phone from these yahoos trying to buy my house does piss me off, but not enough to ban their business model

Fiddling with ownership rules will not do anything for housing affordability. The reason prices are rising is that there is not enough housing being built and has little or nothing to do with who owns the homes. Many cities have myriad restrictions on home construction -- from outright limitations on new building permits to growth boundaries to onerous permitting rules -- while at the same time we subsidize demand through government mortgage insurance and the most lenient mortgages in the Western world (the bank can only take your house, not your other property if you default). There remains much local support for housing restrictions -- you can think of many cities as a cartel of homeowners protecting their monopoly through restrictions on adding competing supply.

There are two financial reasons people want to own rather than rent houses (beyond an array of emotional ones)

Mortgage interest is deductible on taxes, rent is not. Why not equalize these, either by ending the deductibility of mortgage interest, or since that is likely a political non-starter, by making rent payments deductible?

Historically home equity has been a good investment for many, with real home prices doubling over the past 50 or so years. Over this same period, someone with a 90% Loan-to-Value (LTV) would have seen a 10x increase on their 10% equity portion. As discussed above, this is mainly due to subsidizing demand and restricting supply. However, this only works when housing prices grow faster than inflation, which is what people are now complaining about. You can't have both -- either house prices rise faster than inflation and are a great investment or they don't and are more affordable but not a very good investment.

There is no way the President should have the power to mandate this. Republicans are really, really going to regret these precedents when the next socialist-Democrat is in office and mandates something like national rent control.

There is one simple answer to why housing costs rise faster than inflation and incomes -- restricted supply mated with subsidized demand. In many locales the supply of housing is restricted by the government (rent control, growth limits, expensive and time-consuming permitting, etc) and in every part of the country housing is subsidized by the government (mortgage loan guarantees, tax deductibility of mortgage interest, section 8 housing vouchers, etc). The net result HAS to be rising rents and home prices.

I bring this up because we are in the insane situation that both the Left and Right are proposing to attack housing affordability by.... subsidizing demand and restricting supply. Trump's idea is to extend government mortgage guarantees to 50-year mortgages. All this is likely to do is increase the prices of houses to absorb the new lending limits. We saw this in another sector -- college tuition -- where there is hugely subsidized demand and increased student loan limits led to almost one for one increases in tuition.

The Left -- from LA to NY -- is advocating for the same thing it always advocates for: rent control. Rent control is a boon for current renters who have their rents locked in at unreasonably low rates but is a disaster for new entrants to the rental market because the construction of new rental properties drops significantly with rent control (actually the supply can go negative as current rentals are converted to owned units). Rental rates are nominally kept in check but homelessness soars. In addition, rent control has the under-appreciated harm of reducing labor mobility, as one cannot afford to move out of a rent-controlled unit to seek better employment.

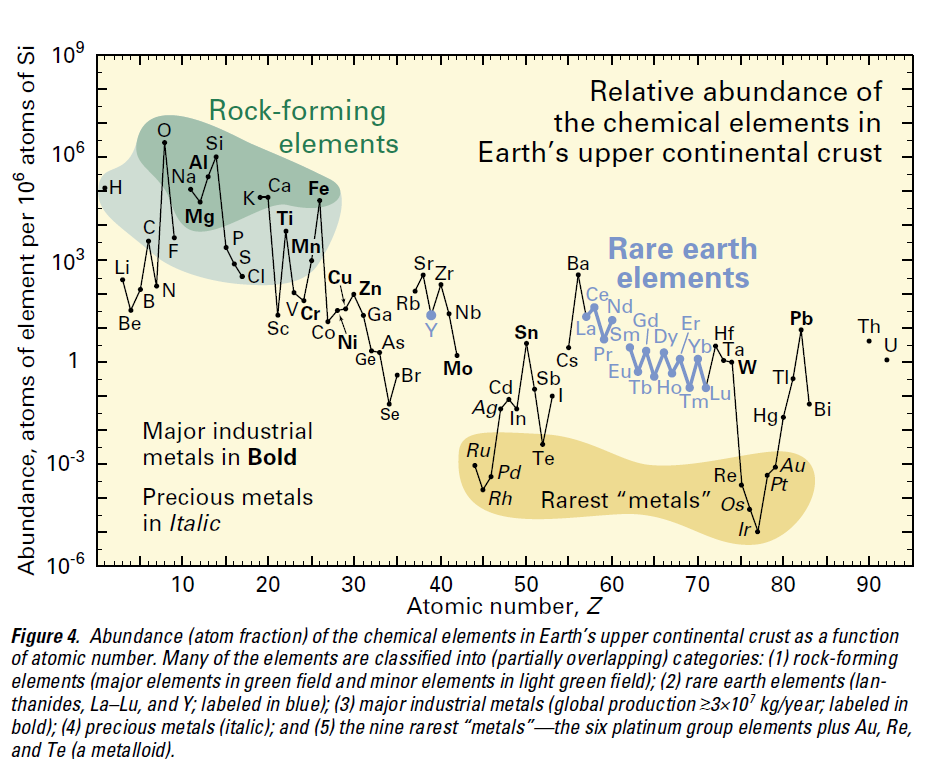

As has been said by many commentators, rare earths are not particularly rare. Via source, here is an estimate of their abundance in the Earth's surface:

Note by the way the Y-axis is logarithmic so small changes in vertical position can mean a factor of 10 or more difference in concentration. But the rare earths are not unreasonably far off fairly common industrial metals like lead, nickel, copper, and molybdenum and well more common than gold, silver, and mercury.

I am not a geologist but my gut feel is that there are plenty of rare earths in the US. The problem is that the process of mining and concentrating the minerals is ecologically relatively expensive -- often large strip mines are involved with a lot of tailings and waste and sometimes dangerous chemicals used in the concentration process. By the time some of these materials starting coming in demand, most companies had written off the US as a viable place to even look -- why bother exploring if you are never going to be permitted to produce anything. Thus much of the world's production has been outsourced to countries like China and poor nations in Africa (or the worst of all worlds -- Chinese mines in Africa) that don't necessarily give a sh*t about the environment.

From an environmental standpoint, this is actually a terrible situation. The US has more wealth and a fair amount of will to take environmentally sensible approaches, so exporting the nasty stuff is not a great long-term solution. California by the way is the worst about this, intent on kicking out everything from coal-fired electricity generation to oil refining from the state but happy to buy the products of these industries from less environmentally-sensitive areas.

Yes, I know. A meltdown in subprime auto loans has been predicted almost every year of the past decade. I am not an economist or stock analyst, so take all this with a shaker of salt, but here is the new factor that I don't think is being discussed much in the context of subprime auto loans: the end of student loan forgiveness:

The U.S. Department of Education announced it will restart interest accrual for student-loan borrowers in the Saving on Valuable Education (SAVE) plan, starting from Aug. 1, according to a July 9 Education Department (ED) statement....

According to the ED, 42.7 million borrowers currently owe $1.6 trillion in student debt.

“Only 38 percent of borrowers are in repayment and current on their student loans,” the ED said in April.

“Most of the remaining borrowers are either delinquent on their payments, in an interest-free forbearance, or in an interest-free deferment. A small percentage of borrowers are in a six-month grace period or in-school.”

The SAVE plan only includes 7.7 million of these borrowers, about 1/3 of delinquent borrowers, but its termination demonstrates this Administration's commitment to end forbearance for delinquent borrowers. Over the last 6 months many other student loan borrowers have been taken off of variouis deferral agreements and asked to pay what they owe.

The reason this is relevant to auto loans is this: there is a large overlap between households with student loans, particularly those with non-performing student loans, and those with sub-prime auto loans. Borrowers delinquent to both a bank for auto loans and to the US government for their student loans will quickly learn that only one of these lenders has the legal power to force their debt to the top of the debt repayment stack.

I am not a financial analyst so I am not sure who would be most hurt by this -- certainly I would not want to be long the equity tranches of securitized auto loans. There are banks such as Ally Financial that have a large percentage of their income in auto loans, including sub-prime, And there are situations like Carvana, which is complicated right now. On the positive side Carvana** stock is way up, likely in anticipation of rising used car sales and prices due to Trump tariffs. On the negative side they are a huge sub-prime auto lender (short-sellers argue that their car sales business is just a loss-leader for their auto lending business).

**Postscript: Carvana is one of those battlefield stocks where super-bulls and super-bears (the later now including Hindenburg Research and Chanos) duke it out constantly. I will mostly stay away as I have already been sucked for years and years into the mother of all battlefield stocks (Tesla). But I will say on Carvana that there may be an interesting pattern emerging. Several years ago the founding family the Garcias sold billions in stock at the top, right before it crashed 99%. Now that the stock has climbed back to those old highs again, the Garcias are selling billions more. It is normal for founders to sell more than they buy to diversify their holdings, but their timing as historically been spectacular.

I am beyond disappointed in folks on the Right who spout what they must know -- or at least knew 6 months ago -- to be economic drivel. It has been a rough ten years as a libertarian -- first abandoned by our natural allies on the Left on issues like Free Speech and now abandoned by our natural allies on the Right on free markets.

Conservatives are saying that criticism of Trump's tariffs causing inflation are overblown because there was not much inflation in April and May. But the reality is that the vast majority of companies have not modified prices to take into account tariffs on their inputs. One reason is that the on-again-off-again nature of these Trump tariff proposals have caused companies to hold their prices for now, eating any cost increases in their profitability but hoping the tariffs will go away (update:PPI Shows Companies Eating Tariff Costs, Bloomberg Finds). No one wants to lose market share by being the first to raise prices (think of Apple vs Samsung on phones, for example). If it becomes clear that tariffs are here to stay in some sector, then you will start to see price increases because companies may eat the costs for one quarter but cannot do so indefinitely.

Here are my two predictions if the tariff uncertainty continues

You are going to see some shortages of product this Christmas. My son works for a major retailer that imports a lot of product and they are struggling with Christmas ordering, which basically has to happen now but is being bought at forward prices that, given tariffs, no one can guess at. I think the net will be reduced buying, lower retail sales, and higher prices this Christmas

Manufacturing investment is going to start falling. It has already flattened somewhat and I would expect 2Q and especially 3Q to be down. Like many economic indicators, there is a lot of lag -- spending this quarter was likely approved and planned long before Trump every got into office. But the crazy shifting tariff situation makes it impossible to plan one's supply chain and manufacturing strategy. My guess is that everyone is going to hold off spending until things are clearer. As to Trump's arguments that the whole point of tariffs is to spur manufacturing investment, most US manufacturers can't get the labor they need already. It's not clear many companies have realistic re-shoring options.

US Manufacturing Expands For Second Month Under Trump, Driven by Stronger Demand and Policy Shifts

In the body of the story they write:

After years of stagnation, the U.S. manufacturing sector is showing renewed strength under President Trump’s leadership. The latest data signal a reversal from the prolonged contraction during Biden’s term. Businesses are responding to policy shifts aimed at strengthening domestic industry, securing supply chains, and encouraging investment. [ed: no evidence is supplied for this last sentence]

This is an example of a the totally irritating genre of media stories that take the form of "President blames his predecessor for bad economic numbers" and "President takes credit for good economic numbers." Politicians' ability to do this, even when the narrative they use reverses month to month, is just amazing. Biden to the end of his Presidency was blaming Trump for every bad economic story and now, barely 42 days into in term, Trump supporters are taking credit for good economic numbers, even those magically created by time-travelling Trump in the first 20 days of January.

This connection between Jan/Feb manufacturing numbers and Trump is dead wrong for two reasons

The economy does not work this fast. The economy is a massive river like the Mississippi where changes in flow in Minneapolis won't be seen for quite some time in New Orleans. In particular, manufacturers are producing to orders they received weeks or months ago for customers in turn who likely are responding to orders and demand they saw even further in the past. If they are sourcing from overseas or selling overseas the delay is even longer. And negative things flow through more slowly than positive. I suppose the President on January 20 could order the CEO's of the 3 largest companies in America put up against a wall and shot and we might see the panic in the economic numbers by March 3, but I am not even sure of that.

I can say with total confidence -- having been a strategic planner at the top levels of Emerson Electric, Honeywell, and AlliedSignal -- that there are very few manufacturing companies in the last 60 days who have been racing to expand their business. The chaos of Trump's changing tariff demands is making planning impossible. Again, nothing changes quickly and projects in progress have to be finished, but I guarantee no one is starting new capital investments in manufacturing that they can defer. Everyone is frozen. And anyone doing business with the government or who needs Federal approval of permits is totally frozen as well because none of that work is getting done. Even if we give Trump the benefit of the doubt to say his intention is to streamline permitting and approvals, right now it is total gridlock. In government offices right now, it is gridlock where everyone has walked away from their cars. I think it is a total lock that we are going to see a dip in manufacturing investment in the coming months.

Economists have given this chaos the name "regime uncertainty" and among many free market economists exactly this sort of shifting regulatory environment under FDR gets part of the blame for the length of the Great Depression. Alex Tabarrok has more here.

This was originally posted on 2-1-25 but was lost in a server update.

Trump's first few weeks have been a mix of good and bad for this libertarian, all against a backdrop of horror at how Imperial the presidency has become. But as of today, perhaps the most destructive and stupid initiative has begun:

Because we are all tired of those fentanyl-toting Canadians crossing the border illegally. I mean, we all saw the Proposal and know how all those Canadians are trying to cheat US immigration law.

Seriously, this is beyond awful -- and not just because of the threat of retaliation, though that is real. Even if all the affected countries roll over and accept these modified tariffs without response, this is still a terrible step for the US. No matter how Trump and his very very small group of protectionist economist friends sell this, this is a tax on 300 million US consumers to benefit a small group of producers. I don't have time right now to give an updated lesson on free trade -- that will have to wait for when I am not on vacation. But I will offer a few ironies:

After campaigning hard on inflation, Trump is slapping a 10-25% consumption tax on foreign goods. That is a straight up consumer price increase for a variety of key products including much of the lumber we use to build homes, a lot of our oil and gas, a lot of our grain and beef, and many of our cars and appliances.

Much of this inflation is going to disproportionately hurt Trump's base. No one is going to care much if a Hollywood actor has the fair trade coffee they buy at Whole Foods go up in price, but Trump voters are going to see a direct effect of this on prices at Wal-Mart.

Republicans have spent 4 years (rightly) condemning Federal and State governments for the economic disruptions of COVID lockdowns and restrictions. While some of the inflation of the last 4 years was due to ridiculously high government deficits, another major cause was the COVID supply chain disruptions. And now Trump is voluntarily recreating them.

The only small hope I have is that Trump is steeped from his business career in a certain style of brinksmanship bargaining that consists of taking an entirely destructive and irrational position in hopes that they folks on the other side of the table will back down and give him more than he should. My son won poker tournaments like this because he would do so much crazy stuff that no one at the table wanted to challenge him. I have always said that I don't think Trump is a particularly good business person -- he has run business after business that has failed. But he is a good negotiator, and has exited numerous bankruptcies with his creditors giving him far more than one would think was necessary.

So I am sure his supporters would say that this is no different from the Columbia situation, when the Columbian president backed down quickly on not accepting repatriation of Columbian nationals under a storm of Trump threats. Perhaps. But even if this stuff is reversed, it is incredibly destructive because it is almost impossible for businesses to plan and make long-term investments when something so fundamental as tariff rates is changing so quickly and arbitrarily.

But there is yet another harm. I know some folks are exhausted with the idea of American exceptionalism, in part because it has been a 75-year excuse to send our military bumbling around the world intervening in every conflict large and small, frequently overthrowing states only to have the replacement be even worse.

But there is one part of American exceptionalism that is important -- our example and our persuasion is a key support beam in upholding two great benefits for humanity -- free speech and free trade. Every government official anywhere is a potential tyrant (if you think that is extreme, I would argue that this exact fear was one of the fundamental founding ideas behind our Constitution). And tyrants want to have their opponents shut up and they want to shift economic activity to reward their supporters. They love censorship and protectionism.

As such, in every country of the world, there is a tremendous headwind against free speech and free trade. There is some natural gravity affecting government behavior that if there is not a constant, visible pressure to maintain free speech and free trade, they begin to be undermined. And at least since 1945, the US has been the primary source of that pressure (one might add the UK to this, at least once upon a time, but looking at them now that is pretty much over).

Over the last 10 years, it has been incredibly depressing to see the US start to lose its commitment to free speech, particularly on the Left which has here-to-fore been the natural home of its defenders. Trump and his supporters say things that seem like a positive step in returning to free speech, but I am a cynical man and I fear that we may only see censorship shifted to different topics rather than actually eliminated. Time will tell, and I will have more on that later.

But in the case of trade, it is the Right in the US that has been the natural defender of free trade. To see the Right not only abandon the defense of free trade, but actually start ramming torpedoes into its sinking carcass, is perhaps the most depressing part of Trump's order.

We begin with the governor of Florida who has just signed an anti-price-gouging law. We talk about how everyone hates price-gouging after a disaster. What could be worse, right?

We then talk about a woman who spends most of her time at home, but rushes out to fill her gas tank right after the storm hits. She has to wait in line for gas for 2 hours because everyone else has done the same as she, racing to the station, but she doesn't mind because she doesn't have anything else to do and feels better. If asked if she would have topped off her tank if the price jumped to $6 from $3, she says no way.

Then we have an owner of a roofing company enter the fray. His men are working 14 hours a day to put roofs on houses. He is making a lot of money, and doing a lot of good as well. Nothing is more important to people than fixing the roof before the next rain. He may be the most important man in Florida at that moment. But he can't keep up with demand, and worse, his guys are having to sit for 2 hours at a time to fill up their company trucks, when they should be repairing roofs. He would gladly pay $10 a gallon if he could just keep his men on the job and not in gas stations.

So at this point we discuss "fairness". It seems fair not to raise prices to "take advantage" of a disaster. But is it fair to allocate gas away from the busiest and most productive whose time is most valuable to the people who are least productive and have the lowest value for their time? We discuss how price caps shift rationing from price to queuing, and the people who get the product shift from those who most value it to those who assign the lowest value to their own time.

Finally, we discuss a guy in Georgia who has a tanker of gas he was going to send to a station in Atlanta. They need the gas more in Florida, but they aren't paying more for it under the new price-gouging law, and so with his higher costs of driving all the way to Florida vs. Atlanta he is going to sell the gas in Atlanta. If the price of gas in Florida were to rise to $6, he would send his truck of gas to Florida in a heartbeat.

This is the kind of discussion we have. We will end up in a debate, with kids pointing out all kinds of things -- eg poor people who have a life or death need and might be shut out at $6. We don't try to resolve things, but want them to understand there are unseen consequences to actions like price-gouging laws that must be considered along with the seen. They may end up dismissing the unseen as less important than the seen, but it should not be ignored.

At the age of about 60, my wife began having terrible pain in her hip. For about a year, this greatly limited her ability to walk longer distances. One of her great joys, exploring new places on foot, was suddenly impossible to pursue. And then the pain got so bad that she could barely sleep, making her life pretty miserable. Projecting forward years or even months, at the pace things were getting worse, it is hard to imagine any sort of reasonably enjoyable life. In any other era in the history of human beings, her life would have been effectively over.

But in her case it wasn't. She had a relatively routine operation where the doctor cut into her leg, carved out a large part of the femur and socket joint, and replaced it with a contraption of titanium, cobalt-chromium, ceramic and plastic. Sixty years ago this operation was unheard of, and 100 years ago many of the materials used were unknown. But now we do it routinely. I have a partial knee replacement that is only weeks old and walked 3 miles on it this morning. It is unusual for me to meet anyone my age or older who doesn't have some sort of prosthesis, whether it be a joint replacement or a heart stent or a pacemaker. What we all have in common is that a century ago our lives would likely either be literally over or at least so painful we might wish it were so.

This may seem like an odd way to restart my blogging, but before I spend the coming months and years criticizing everything and everyone, it is worth remembering that we live in the greatest time in human history. The median human experience in all of history is miserable subsistence poverty. At least until the recent explosion of wealth and mass escape from poverty that has characterized the last 75 years, the 95th percentile human experience was probably subsistence poverty. Everyone alive today is probably in the top 10% or even 1% of historical humans in terms of income and well-being. This is even more so for a resident of the US, where even a person on the poverty line in the United States today, say around the 20th percentile of income, is likely in the 80-90th percentile worldwide.**

One house has hot and cold running water, central air conditioning, electricity and flush toilets. The other does not. One owner has a a computer, a high speed connection to the Internet, a DVD player with a movie collection, and several television sets. The other has none of these things. One owner has a refrigerator, a vacuum cleaner, a toaster oven, an iPod, an alarm clock that plays music in the morning, a coffee maker, and a decent car. The other has none of these. One owner has ice cubes for his lemonade, while the other has to drink his warm in the summer time. One owner can pick up the telephone and do business with anyone in the world, while the other had to travel by train and ship for days (or weeks) to conduct business in real time.

I think most of you have guessed by now that the homeowner with all the wonderful products of wealth, from cars to stereo systems, lives on the right (the former home of a friend of mine in the Seattle area). The home on the left was owned by Mark Hopkins, railroad millionaire and one of the most powerful men of his age in California. Hopkins had a mansion with zillions of rooms and servants to cook and clean for him, but he never saw a movie, never listened to music except when it was live, never crossed the country in less than a week. And while he could afford numerous servants around the house, Hopkins (like his business associates) tended to work 6 and 7 day weeks of 70 hours or more, in part due to the total lack of business productivity tools (telephone, computer, air travel, etc.) we take for granted. Hopkins likely never read after dark by any light other than a flame.

If Mark Hopkins or any of his family contracted cancer, TB, polio, heart disease, or even appendicitis, they would probably die. All the rage today is to moan about people's access to health care, but Hopkins had less access to health care than the poorest resident of East St. Louis. Hopkins died at 64, an old man in an era where the average life span was in the early forties. He saw at least one of his children die young, as most others of his age did. In fact, Stanford University owes its founding to the early death (at 15) of the son of Leland Stanford, Hopkin's business partner and neighbor. The richest men of his age had more than a ten times greater chance of seeing at least one of their kids die young than the poorest person in the US does today.

You don't even have to go back to the 19th century to find high childhood death rates. Both my mom and dad (who were born in the 1920s and 1930s) lost a brother when they were young to disease, both whooping cough I think. My dad contracted polio as a teen and never regained full strength in one leg. They both talked about these things like they were so normal -- I am sure it was a tragedy for the families but a sort of normal and expected tragedy.

Most of the issues that have people convinced that everything is awful are not so daunting when viewed on a historic scale.

The environment? The air in cities is immeasurably cleaner than when I grew up (I remember smog so think in LA you couldn't see anything). Water quality is better, litter has almost completely disappeared (at least compared to when I grew up). The thing that never really gets mentioned in lovely period pieces like Bridgerton is just how bad everything smelled and how dangerous the water was. Today, we tend to be arguing over smaller and smaller concentrations of smaller and smaller risks. There is the climate issue of course, but many of the disasters blamed on climate change are historically typical and have little to do with warming temperatures (starting with the LA fires). We will get back to climate in due course.

Or take the issue of race. Growing up in the South in the 1960s and 1970s, the improvements we have seen in race relations, at least until about 2000, were remarkable. Tribalism and xenophobia are too wired into humans to purge entirely, but to a remarkable extent in the US we had limited overt racism to the low status fringe. Another generation or two and we were well-positioned for a truly race-blind society. [We have unfortunately lost ground on this in the last 25 years, as racism and anti-semitism seem to have re-emerged in high-status groups from a toxic mix of marxism and falling academic standards. But I have hope]

This is not to say that life doesn't suck for many people on Earth. Though there are billions fewer than fifty years ago, you could be one of a billion people living in less than $1 a day poverty. You could be a woman living in virtual slavery in Iran, a mother who just wants her kids to survive in Gaza, or a Russian soldier enduring years at war in the Ukraine. But for the vast majority of people on Earth, and for a huge proportion of the people in this county, the Earth is the best world we have ever had. Understanding that, and the connection between our current prosperity and ideas like individual rights, capitalism, free trade and scientific inquiry will continue to be a key focus of this blog.

I am not a Pollyanna -- I see threats and worrying trends in every direction, and will be writing about them. For example, tomorrow we trade a President with an immense set of flaws for another with an immense set of entirely different flaws. Perhaps I am not as disappointed as some by recent trends because I have always treated politicians and the media and academia with immense skepticism, so I am less surprised by their obvious failings. I have always expected people in power -- government, corporations, wherever -- to abuse their power and believe the trick is to wire the system in a way that they cannot do too much damage. In preparation for blogging again, and looking back over my old writing, one consistent theme I see is a disdain for solutions that boil down to "if only we replace their people with our people." That's a hopeless approach. We have flip-flopped the Coke and Pepsi parties in power more times in the last 50 years than we did in 100+ years before that, and its not making things better. If anything its escalating a tit for tat power grab as each new administration pushes the precedent frontier forward more toward Presidential authoritarian power. This is not a secret: Trump is bragging about it.

One of my first long-form posts will be on the breakdown of the US political consensus around free speech and free trade. Both concepts have been critical to the prosperity I write about above, but both are concepts politicians tend to shy away from (free speech allows their opposition to speak out and potentially remove them from power, while free trade limits the economic spoils they can dole out to powerful labor and business supporters). To a large extent, US moral and intellection leadership post WWII on free speech and free trade has been critical to keeping these concepts alive around the world against the headwinds of authoritarianism. Now, with a breakdown of support in the US for both, one wonders what future they have. More later....

**footnote: It is remarkably hard to get the data to do this analysis. Everyone that collates income inequality data wants to show the US as awful so they will compare US only with the US and not with any other countries. This chart is the closest I have found recently and actually seems to say that the US 20th percentile is about at the world 65th percentile. But this underestimates the US position since it uses the other major trick of poverty stats -- it omits the effect of taxes and government transfer programs. No one ever believes me when I tell them, but most poverty stats, including the US poverty line, are based on income without transfers, ie BEFORE the effect of anti-poverty programs. The stats thus always show no progress on poverty and argue for more government anti-poverty programs while excluding the effect of existing anti-poverty programs from their data. On a world scale US anti-poverty programs are robust, and we have (again against perceptions) one of the most progressive tax codes anywhere so with the effect of anti-poverty programs my guess is that the US 20th percentile is over the 80th percentile worldwide. I took a shot at this analysis vs Scandinavian countries quite a while ago here. When I have a chance, I will see if there is newer raw data available,/footnote

So a $15 national minimum wage will almost certainly be on the table in Congress this year, and if past such legislative efforts are any guide the Republicans will probably eventually go along in exchange for reducing the $15 to a lower number and slowing the rollout.

I have talked a lot about the negative effects of higher minimum wages on low-skill workers. Two good example background posts are here and here. I covered how a broad range of labor regulation hurts unskilled workers in a cover story for Regulation magazine a few years back. Unfortunately, in a country where the average American buys about $1000 in lottery tickets each year, the willingness to believe we can get something for nothing is strong.

But I want to talk specifically about a Federal minimum wage increase, where one other problem emerges. The best way to state this is -- how can one possibly set the same minimum wage for San Francisco at the same rate as one does for rural Mississippi? Here is one source for comparative state cost of living. Doing this by county would make the curve even wider.

Cost of living in Hawaii is more than 2x that of Mississippi. CA and NY are not far behind. A minimum wage that might comfortably be accommodated in San Francisco (and note even there the rise to $15 was ending service jobs in that city long before COVID), would be an economic disaster for rural Alabama. I don't tend to think primarily along racial lines as seems to be the case on the Left today, but basically this is a policy driven by rich white tech guys in San Francisco that is going to devastate the employment prospects of rural blacks.

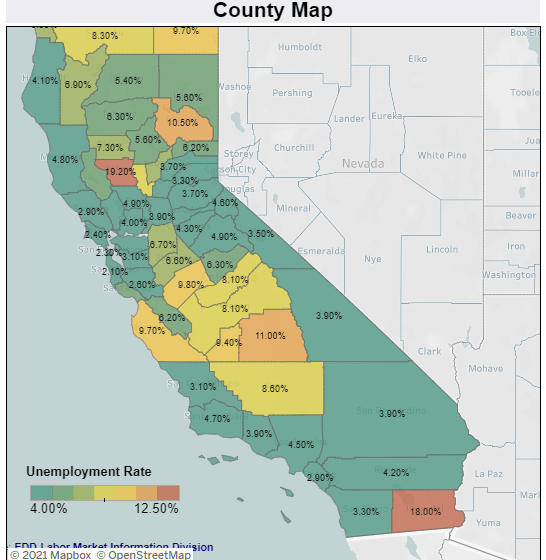

Whatever one's misgivings about minimum wages, it is certainly true that allowing states to take the lead on setting minimum wages (counties would make even more sense) makes a lot more sense that trying to take action at the national level. Even with state action there are disparities. Look at this unemployment map of the rural counties in CA vs. the tech. enclaves in the Bay Area (the chart below is January 2020, I wanted to dial back pre-COVID). Those rural counties are being slaughtered by the $15 minimum wage. Just think about rural areas in states less costly than CA.

So a state by state approach is WAY better. There are three reasons, in increasing order of cynicism, why Democrats in Congress will still insist on a higher national minimum wage.

Democrats in Congress believe they are carrying salvation to the powerless masses in Alabama who are held in slavery by state Republicans. Democracy and the "will of the people as expressed at the ballot box" are only sacred when it's our team in charge.

Folks in Congress did not spend a career fighting to win a seat in that body only to find that there is something that would be best done by state legislators. They didn't work to get promoted to have LESS power (though that is exactly how the country was originally designed). This is the enemy of all Federalist notions

The fact that a $15 minimum wage will devastate many rural areas, mostly Republican bastions, may be a feature and not a bug for some. Think of the $15 minimum wage as Democratic revenge at the heart of red states for the Trump reductions of SALT deductions in the tax code (which were a dagger at the blue state model).

Category: Economics, Regulation |

Comments Off on The Other Problem With A National Minimum Wage -- The National Part

Long-time readers will know that I am interested, to the point of obsession, in incentives. One should always be suspicious of bad outcomes described as irrational or the nefarious actions of bad people. In both cases, if one looks carefully, the outcomes usually turn out to be the perfectly rational outcomes of perfectly normal people responding to bad incentives, assumptions, and/or information.

I personally believe the COVID response in this country (and others) is exaggerated and counter-productive. But for this post I am not going to ask you to agree or disagree with my skepticism. Instead, I am going to focus on incentives, and show how media, academia, and government all have incentives, assumptions, and information asymmetries that push them towards exaggerated COVID responses.

The following list is not necessarily complete and the items here are not independent of each other. Having completed this post, they now look a little random but this is sometimes the way I clarify my thinking on things -- to write and publish and get feedback and maybe be more structured the next time.

Incentives

Political incentives to "do something" about the issue of the moment. We see this after every high-profile "bad thing" that happens. There is immense pressure on politicians to do something -- pass some law (often with a person's name in it) or, if the legislative process is perceived as to slow, fire off some executive order. In the heat of battle these actions are often taken without regard to efficacy, cost, or unintended consequences. In the heat of these frenzies, a multi-dimensional decision is magically redefined as having only one dimension that matters. Anyone who focuses on costs or unintended consequences or even efficacy problems of the proposed solution are cast as heartless and uncaring, potentially even evil and nefarious.

Politicians always legislate to first-order metrics, never second-order metrics. Politicians know that the public and the media is looking at their country or state every day and publishing the number of COVID cases and deaths. No one is publishing the number of additional suicides, or cancer deaths from people too scared to go to the hospital, or increased starvation and disease deaths in poorer countries as food prices rise and aid from rich countries dries up. These second order effects are real but hard to prove or measure. They are what we call "unintended consequences" but should instead call "ignored but entirely predictable consequences."

Political incentives to expand power. Every politician in every branch of government is always working to expand their own power (this is not unique to government, you can say the same thing of executives and functional departments in many large corporations). When the public is scared and panicky, politicians are able to break through past limits and norms and establish new precedents. The best example of this is that governments in Western democracies all expanded their power during the 20th century wars, expansions that largely stuck and were not reversed in peace time (except for a few fortunate examples like locking up whole ethnic groups in internment camps). When the public is scared, power is to be had and it is the unusual politician that will say in such a situation that the right solution is to do nothing.

Political incentives not to admit error. Politicians simply cannot admit error. To some extent this is due to the personality and ego traits that the political process sorts for, and to some extent this is based on day to day political incentives. But think about any President in your lifetime and try to think of even the smallest issue on which they said something like "I tried X, over time X has not worked and now I realize we should do something other than X." We would actually hope this is the kind of person we have leading the country, but simultaneously our own behaviors don't allow it. Presidents frequently admit past errors of others (eg, a current President saying the war in Afghanistan was a mistake) but they can never turn against any policy of their own. So if, say, lockdowns were the response to wave 1 of the virus, lockdowns are damn well going to be the response in successive waves. Because not doing so is essentially an admission that it was a mistake the first time.

If it bleeds, it leads. This one takes little explanation, because I think most of us understand the strong incentives of news organizations to create and amplify emergencies to increase the attention and viewership they get. Cable news had a huge spike in viewership after 9/11 and again in the early days of the Gulf War, and they are constantly jonesing for the same sort of hit. Remember that the media has accurately called 11 of the last 2 pandemics, earlier predicting disaster from swine flu (dating myself here), bird flu, ebola, zika, mad cow, and probably several I can't remember.

Reference to personal circumstances when making national trade-offs. I would say that the number 1 thing that drives me crazy about statists on the Left and Right and which makes me a libertarian is the tendency to impose solutions to tradeoffs on everyone in the country based on how you would personally make decisions for yourself. If one-size-fits-all public policy decisions are going to be made, I want them to be made in a way that suits me. For example, a politician in Chicago might say they would never feel comfortable letting thier kids walk to school on their own, so no parent should be allowed to let their kids walk to school alone. Applying this to COVID, we know there is a large contingent in media, academia, and politics who will say that is is wrong to consider economic damage when evaluating COVID lockdowns. What do all these folks have in common who tend to be advocating strongest for lockdowns? They still have their jobs, are still getting paid, can still be productive over the Internet, and are comfortable getting their social interaction over zoom. Note that these are the same folks that constantly tell us to check our privilege, but then tell us to ignore the economic hardships of lockdowns that they are too privileged to experience. Only by the most extreme action do the voices of the less privileged who are suffering the most under lock-downs get heard (and even then, like the hair dresser in TX and later in SF, they get mocked by the elite).

Assumptions

Trump is so bad that no price is too high to get rid of him. I have told folks for years that every generation thinks their current era is uniquely politically toxic. I don't think we have yet risen even to 1968 levels of discord, but one exception is the hatred for Trump that exists in some quarters. I personally have never seen anything like it. The nadir was when Trump mentioned that HCQ looked like a promising COVID treatment and the governors of MI and NV immediately banned HCQ without evidence to make Trump look bad (a desire I assume stems from a perception that Tump is so dangerous and represents such an existential threat that any action to undermine him or make his re-election less likely should be pursued). A prominent study was essentially made up out of whole cloth to prove HCQ was dangerous and thus Trump bad, a conclusion that should have made zero sense to everyone as HCQ is used by millions every day as a malaria prophylactic. I find Trump distasteful but trust the American system to limit the damage of tyrants, but many are working from a very different assumption.

Humans have conquered nature. I will confess to having an almost Victorian confidence in progress, but even I accept that sometimes nature throws things at us that are a) not our fault and b) we can't yet stop. But throughout our COVID responses there seems to be, particularly in Western nations, an assumption that we should be able to prevent death from this thing -- ie that any death should be judged as a failure of our response. But diseases still kill people. Last year communicable diseases killed at least 15 million people in the world. And many of our Western deaths have been among the very old in care facilities where the average life expectancy pre-COVID was numbered in months.

Information

Good cause skewing of data, or "fake but accurate." Decades ago, there was a stat that there were a million homeless people in the US. Everyone repeated it as gospel. Someone tracked it down, and eventually discovered that it was just made up by a homeless advocate who just picked a round large number. When this was presented to a well-respected reporter on NPR, that the "fact" she was quoting was no such thing, she just shrugged. She said homelessness was clearly a problem and if the number she was quoting (as a reporter!) was exaggerated, then it was in the good cause of increasing attention to homelessness. This was the first example I can remember of something that was considered fake but accurate, but there have been many more since. During COVID, this has caused outlets like Goggle and Facebook to actually censor opinions the tend to be skeptical of the severity of the disease or efficacy of mitigation steps like lockdowns. They claim to be doing so for a good cause, believing it is better to err on the side of having the public too cautious rather than insufficiently cautious.

Asymmetric public exposure to experts. Throughout COVID we have been told that the experts all say X, that there is a consensus for X. And sure enough, we mostly only hear X on the news. But anyone in academia can tell you that this sort of homogeneity of opinion can't possibly be true. As in other science, on issues such as mask or lockdown effectiveness or herd immunity thresholds, academics hold a wide range of opinions and there are a wide range of findings in the literature. But this heterodoxy in opinions never really gets full public view due to media incentives, political incentives, and good cause skewing. The most extreme voices on the end of the academic scale that support the media's and politicians' desire to create fear are selected for public exposure. Then, these selected academics are retroactively crafted into leading experts. Any of you folks every heard of Anthony Fauci before this started? How about whatever expert your governor is using? No, you had not -- these are prominent people in their field but just one of ten or twenty equally qualified persons who could have been selected and presented as experts. They are then retroactively reinvented not as one of ten folks with a wide variety of opinions but as the one leading true unassailable expert.

Social media amplification of tail-of-the-distribution events. One of the features of social media independent of these incentives is that it tends to spread and amplify tail of the distribution events/risks. The problem is that there seems to be two personality types in people -- one, and I would include myself in this -- who are knee-jerk skeptical of such stories. Did it really happen? Did A really cause B? Is this really anything more than one bizarre outlier? But there is a second type of person, and I would say that they are WAY more prevalent than I would have believed a year ago, who sees a story that someone's gynecologist's hairdresser's uncle claimed to have had heart issues after getting COVID and suddenly "everyone who gets COVID has permanent heart damage!" Even before the Internet, Americans were very bad at parsing relative risks and now they just seem terrible at it.

Category: COVID-19, Economics |

Comments Off on Why The Incentives Are Stacked to Overreact to COVID

A couple of years ago I wrote about the 1994 Myra Sadker book "Failing at Fairness," a book that tried to make the case that girls were getting hosed (as compared to boys) by the US educational system. Leaving aside my general sense that all kids of all races and genders are getting hosed by the current public school system, the idea that girls were doing worse in education was already wrong in 1994 and is demonstrably ridiculous today. I showed these charts at the time. First from the indispensable Mark Perry:

In this second chart, even the New York Times has noticed

Really, one only needs to go look at the unemployed knuckleheads living in their parents' house and rioting for Antifa to know we have a boy problem today, not a girl problem. But I wanted to add one more piece of data, from some research I cannot vouch for in Self. The income results for young women are about what you would expect from the education data above, and the crossover (somewhat coincidentally because it is dependent on start date chose) almost exactly matches the crossover in the education data.

Perhaps it has always been so, but we live in a time when our social science mythology is really divorced from social science data.

Category: Economics, Gender |

Comments Off on An Update on the "Failing at Fairness" Gender Myth

A few weeks ago Matt Yglesias published a tweet (since deleted, which I don't totally understand as I thought it was pretty innocuous from a Progressive viewpoint) saying that he wanted to spend more time focusing on "relative child poverty." What the heck is "relative" child poverty? I want to spend a bit of time discussing why this is a useless metric, helpful only if one want to try to sell socialism in the US.

Relative child poverty is a metric based on the country's median income -- how many kids live in families with income that is X% of the median. Here is an example (source):

If you click on the source, the headline presents this as "These rich countries have high levels of child poverty." The implication is that the US has more child poverty than Latvia or Poland or Cyprus or Korea and only slightly less child poverty than Mexico and Turkey. But does it really mean this? No. This chart is a measure of income equality, NOT the absolute well-being of children.

Many of the countries ahead of the US are there not because their poor are well off, but because their median income is so much lower than ours. In fact, you will notice the lack of African and Asian countries in this. I will bet a lot of money that certain countries in Africa and Asia everyone knows to be dirt poor would beat out the US in this, thus making the bankruptcy of this metric obvious.

Take Denmark in the #1 spot. It looks like 20% more kids in the US live in poverty than in Denmark. But per the OECD, the US has a median income 41% higher than Denmark. So what it really means is the US has 20% more kids living under an income bar that is set 41% higher. How can this possibly have any meaning whatsoever, except to someone who wants to make the US look bad?

The chart below does the same thing -- it has nothing to do with absolute well-being, but defines poverty as living below some percentage of that country's median income. In this metric, a country where everyone equally made only $1000 or even $10 a year would have 0% poverty!

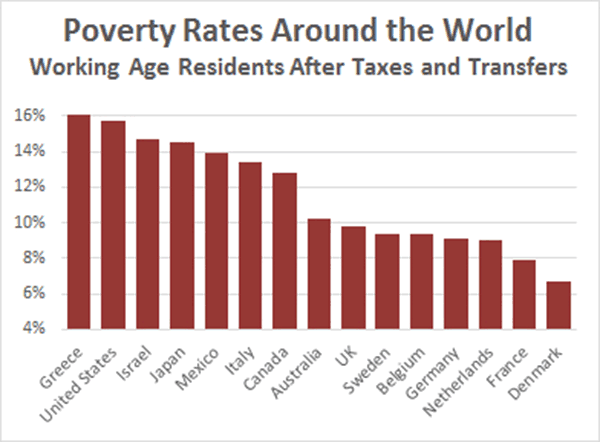

Within the US, the same game is being played with poverty stats. Despite decades of government income distribution and poverty programs, the stats appear to show that the US has nearly unchanged poverty rates. But this is because the census data on which the poverty stats are based EXCLUDE government transfers -- in other words, they exclude the effect of many or most of these poverty programs. When this and other issues are corrected for, US poverty rates have dropped to all-time historic lows (source)

One thing you never, ever, ever see is comparisons of the poor in the US to poor in other countries on an absolute well-being basis after transfer payments. That is because the bottom 10 or 20 percentile in the US are among the top half of richest people in the world, and in many nations they would be among the top 10%. It is possible to make these comparisons, though. I did so several years ago from a data set I saw Kevin Drum using (ironically to try to make the point the US is worse than Europe, again by using relative poverty numbers). I am sorry this data is old, but there is a long time-delay in the data source itself and I have not updated the analysis for a couple of years (on my to-do list, though).

Here are the US Bernie-Socialist favorites Denmark and Sweden:

I know progressives would argue that if you take more from the right end and give it to the left end, our poor would be even better off. But we have a control group for this -- Including Sweden and Denmark -- and that is clearly NOT the result one gets. The problem with this theory is that forcible income redistribution policy and economic growth / prosperity are not independent variables. When you redistribute the pie, you get a smaller pie.

If one wishes to compare poverty across countries, the way to do it should be to compare the disposable incomes after taxes and transfers (adjusted for PPP) of the 10th or 20th income deciles in each country. This seems obvious to me, after all we use the median (50th decile) income to compare prosperity across nations, so why not the same approach for poverty? But no one ever does it. My guess is the point is to exaggerate poverty in the US and understate it in socialist nations.

Well, in 1820, 94 percent of the world’s population lived in extreme poverty (less than $1.90 per day adjusted for purchasing power). In 1990 this figure was 34.8 percent, and in 2015, just 9.6 percent.

In the last quarter century, more than 1.25 billion people escaped extreme poverty - that equates to over 138,000 people (i.e., 38,000 more than the Parisian crowd that greeted Father Wresinski in 1987) being lifted out of poverty every day. If it takes you five minutes to read this article, another 480 people will have escaped the shackles of extreme of poverty by the time you finish. Progress is awesome. In 1820, only 60 million people didn’t live in extreme poverty. In 2015, 6.6 billion did not.

Category: Economics |

Comments Off on The US Has the Least Poverty In the World -- Here Is How Metrics Are Crafted to Hide That Fact

For this post I just wanted to make a more narrow point -- one reason that unicorns (private startups with valuations north of $1 billion) like WeWork and Uber and Peloton had their valuations get so out of whack is because there is no way to short stocks in the private equity world.

Companies like Lyft and Uber and WeWork have seen private funding rounds at ever-increasing valuations. These are done outside the accountability of the broader market and untethered to any sort of normal valuation metrics like earnings or even revenues.

Lots and lots of investors, perhaps the vast majority of them, believed that the last private round that valued WeWork at $45 billion was insane. Many folks, including myself, would have gladly shorted the stock at this price had we been able. Heck, many of us would have shorted back at $10 and $20 billion valuations for the company. Because there is no short selling in this private equity world, unicorn valuations are +based on information from a very limited number of the most optimistic company supporters. And because of this faulty price discovery, billions of capital that could be doing something more productive have been wasted in many of these companies, poured into business models that don't work or, worse, the tequila and drug fueled Gulfstream flights of the founders.

At the start of the bubble, a particular asset (be it an equity or a commodity like oil) is owned by a mix of people who have different expectations about future price movements. For whatever reasons, in a bubble, a subset of the market develops rapidly rising expectations about the value of the asset. They start buying the asset, and the price starts rising. As the price rises, and these bulls buy in, folks who owned the asset previously and are less bullish about the future will sell to the new buyers. The very fact of the rising price of the asset from this buying reinforces the bulls' feeling that the sky is the limit for prices, and bulls buy in even more.

Let's fast forward to a point where the price has risen to some stratospheric levels vs. the previous pricing as well as historical norms or ratios. The ownership base for the asset is now disproportionately made up of those sky-is-the-limit bulls, while everyone who thought these guys were overly optimistic and a bit wonky have sold out. 99.9% of the world now thinks the asset is grossly overvalued. But how does it come to earth? After all, the only way the price can drop is if some owners sell, and all the owners are super-bulls who are unlikely to do so. As a result, the bubble might continue and grow long after most of the world has seen the insanity of it.

Thus, we have short-selling. Short-selling allows the other 99.9% who are not owners to sell part of the asset anyway, casting their financial vote for the value of the company. Short-selling shortens bubbles, hastens the reckoning, and in the process generally reduces the wreckage on the back end.

I am not advocating some goofy plan to bring short-selling to private equity. What I am saying is that prices set in markets with a robust ability to sell short are going to be much more trustworthy than prices set where short-selling is not an option.

Category: Economics, Investing |

Comments Off on Unicorns and the Societal Benefits of Short Selling

Q I can read you the tweet, Mr. President. You said that, “Badly run and weak companies are smartly blaming these small tariffs instead of themselves…”

THE PRESIDENT: Yeah. A lot of badly run companies are trying to blame tariffs. In other words, if they’re running badly and they’re having a bad quarter, or if they’re just unlucky in some way, they’re likely to blame the tariffs. It’s not the tariffs. It’s called “bad management.”

The first answer to this is, LOL. This is the man with a string of failed businesses (steaks, college) and multiple bankruptcies in his core business. In fact, I would list one of Trump's most useful business skills is his ability to get other players in the capital structure to take the losses for his bad business decisions and management.

But as far as trade is concerned, if one is worried about bad management in US businesses, then the right thing is certainly not to protect those businesses from competition. The US auto business in the 60's and 70's as well as almost the entirety of the British industrial base in the 20th century are good examples of the problem. Protecting businesses from international competition, as is Trump's objective, only shelters those businesses from accountability and reduces the pressure to fix whatever bad management may exist.

As a special bonus, I would argue that many of the bad habits of large US companies today are directly attributable to the stimulative Federal Reserve policy which Trump wants to increase. Returning profits to shareholders in the form of share buybacks rather than dividends is a perfectly valid strategy, particularly when the tax code favors capital gains over dividends. But when companies borrow billions just to buy back more of their own stock, rather than reinvest it in new opportunities, something is broken. A large part of the blame are twin Federal Reserve policies of low interest rates and a QE-created equity and asset price bubble.

Apparently California is close to a new law mandating that Uber drivers (and other "gig" economy workers) be treated as employees rather than independent contractors. Progressives are cheering this as a victory for the drivers:

Billionaires who say they can’t pay minimum wages to their workers say they will spend tens of millions to avoid labor laws. Just pay your damn workers! https://t.co/PtyP4JZ7W0

I have explained before why this will likely kill Uber (e.g. here) but let me summarize quickly the argument of why this is bad for most drivers (self-plagiarized from a Twitter thread). The key issues are driver productivity and driver agency.

Let's define worker productivity as far as Uber is concerned as the amount of customer revenue a driver brings in per paid hour. In the current model, this is not a real concern for Uber as they are only paying Uber drivers when they are actually driving customers. Essentially, Uber drivers and Uber have a revenue share agreement to split customer revenue. Uber has set the share low enough to maximize its revenue (of course) but high enough to still attract drivers. It tweaks this formula fairly frequently. Uber driver productivity as we have defined it is essentially locked in by the formulas in this revenue share agreement.

Given this arrangement, note what Uber does NOT have to worry about. It does not have to worry that drivers are working hard enough or are positioning themselves in productive locations and productive times of day. Uber drivers can drive anywhere they want at any time they want. An Uber driver currently can turn on the app at 4am in the suburbs of Peoria and Uber does not care, even if this positioning is unlikely to get many rides. Why? Because Uber only pays if there is a ride. It doesn't care if the driver is sitting around unproductively, because it is not paying the driver for that time.

So today, it is left up to the driver to make trade-offs between the most productive time & positioning and the demands of their own personal schedule & life choices. This sort of flexibility has real value to many drivers. It is agency that many hourly workers don't have, and that has attracted many people to become Uber drivers. My neighbor, for example, sits in his living room all day with the app on and runs out to the car whenever he accepts a ride (and then turns the app off so he can come back home). He gets few rides in our area but he is happy with the lifestyle and the little bit of extra money he makes from Uber.

But this all changes if drivers must be Uber employees and subject to wage and hour laws. The key difference under such wage and hour laws is that Uber would have to pay drivers whether they have a passenger or not, as long as the app is turned on. Suddenly, forced to pay for labor whether the labor is working or not, Uber is going to get real interested in driver productivity.

If Uber pays by the hour, my neighbor's preferred way to drive is a dead loser for the company. In fact, if I am a driver and paid by the hour, I could go find a library in an out of the way place at an odd time of day and sit and read and collect hourly paychecks -- All without having to drive much. Now, instead of productivity choices being in the driver's hands because it's the driver that makes more or less money with greater or lesser productivity, these choices now land in Uber's lap. Uber can no longer allow so much driver agency.

If making Uber drivers hourly workers does not kill Uber altogether, then Uber is going to be forced to monitor driver productivity and do one or both of two things:

Establish productivity rules, such as driving time windows and allowed geographic ranges and/or

Set a minimum productivity threshold below which Uber will have to let those drivers go

Interestingly, like a lot of labor regulation, this one will benefit the middle while hurting the lower-paid drivers.

Top drivers will be unaffected, because they already make the minimum

Middle drivers may get a small boost

Lower-earning drivers will lose their driving jobs entirely

A better way to characterize this law is that it will greatly reduce the flexibility many Uber drivers love, while causing the lowest paid drivers not to make more, but to lose their driving gig altogether.

Tyler Cowen pointed out this article on the widening gap between white and black home ownership rates. Black home ownership rates have fallen pretty steadily since the financial crisis -- apparently when banks are castigated by activists and government officials for "exploiting" blacks by giving them easy credit, blacks no longer get as much easy credit.

For people trying to rise in their economic status, there are a lot of things wrong with home ownership. The most important is that it limits geographic flexibility. Home owners have much higher costs to pick up and move, making it harder and less likely to exploit opportunities for better work and/or lower living costs in other parts of the country. And as someone who just had an $8000 air conditioning unit fail in 110 degree heat, I can testify that home ownership also involves more risk of large unexpected expenses than does renting. All things considered, in a free market, there are a lot of reasons home ownership might be a bad idea for folks trying to rise in income.

The complicating factor, as usual, is it is not a free market. Public policy has tipped the scales such that home ownership has become probably the most important of all middle class savings vehicles. Part of this is a human behavioral issue -- people contribute to homes every month because the bank makes damn sure that they do so (sort of like having a really tough personal trainer). No other savings vehicle has such strong incentives not to cheat on monthly contributions. But even so homes would still not be such a great investment vehicle. In a 30 year mortgage, the percentage of your monthly payment in the early years that goes to equity is trivial. There is really no reason that a home should be anything more than a depreciating asset, like a car or a boat.

Which brings us to the public policy angle -- a myriad of policy interventions all conspire to make sure that home prices rise continuously. On the demand side, demand is subsidized via special government mortgage programs, special treatment for mortgages on bank balance sheets, the mortgage interest tax deduction, as well as a number of direct subsidies for lower income folks. We even had QE where the government was buying up mortgage bonds to keep interest rates low. On the supply side, supply is constrained through growth boundaries, density limits, zoning restrictions and a zillion other local regulations. The net effect of this subsidized demand and constrained supply is (with a few interruptions) ever-rising prices.

While many of us decry crony capitalism, most every homeowner in this country (including me) is a crony. We benefit from this program that like most all other crony capitalist programs, benefits incumbents at the expense of new entrants. In this case, those of us with houses get to enjoy a good rate of return on our home investment while those without homes are shut out of the market by rising prices.

I want to put a couple of caveats on this post. 1) Though there are utilitarian arguments related to slavery in this post, by no means do I think they ever come close in magnitude to the basic fact of the moral outrage of slavery. 2) Though there are utilitarian arguments about reparations in this post, by no means do I think they ever come close in magnitude to the moral outrage of penalizing people for sins of their grandfathers.

The other day, in what I thought was a quick throwaway comment on Twitter to an NBC article that seemed to be supporting slavery reparations, I wrote

Hmm, pretty sure my family in Hamburg, who were pre-occupied in the late 19th century with getting out from under Prussian rule and heading for America, did not benefit from US slavery

One response I got which I want to address was this one:

Yes they did. They left their home country and came to America because the abundance of opportunities. Opportunities made possible by the years of free labor take a wild guess from who?

This notion that slavery somehow benefited the entire economy is a surprisingly common one and I want to briefly refute it. This is related to the ridiculously bad academic study (discussed here) that slave-harvested cotton accounted for nearly half of the US's economic activity, when in fact the number was well under 10%. I assume that activists in support of reparations are using this argument to make the case that all Americans, not just slaveholders, benefited from slavery. But this simply is not the case.

At the end of the day, economies grow and become wealthier as labor and capital are employed more productively. Slavery does exactly the opposite.

Slaves are far less productive that free laborers. They have no incentive to do any more work than the absolute minimum to avoid punishment, and have zero incentive (and a number of disincentives) to use their brain to perform tasks more intelligently. So every slave is a potentially productive worker converted into an unproductive one. Thus, every dollar of capital invested in a slave was a dollar invested in reducing worker productivity.

As a bit of background, the US in the early 19th century had a resource profile opposite from the old country. In Europe, labor was over-abundant and land and resources like timber were scarce. In the US, land and resources were plentiful but labor was scarce. For landowners, it was really hard to get farm labor because everyone who came over here would quickly quit their job and headed out to the edge of settlement and grabbed some land to cultivate for themselves.

In this environment the market was sending pretty clear pricing signals -- that it was simply not a good use of scarce labor resources to grow low margin crops on huge plantations requiring scores or hundreds of laborers. Slave-owners circumvented this pricing signal by finding workers they could force to work for free. Force was used to apply high-value labor to lower-value tasks. This does not create prosperity, it destroys it.

As a result, whereas $1000 invested in the North likely improved worker productivity, $1000 invested in the South destroyed it. The North poured capital into future prosperity. The South poured it into supporting a dead-end feudal plantation economy. As a result the south was impoverished for a century, really until northern companies began investing in the South after WWII. If slavery really made for so much of an abundance of opportunities, then why did very few immigrants in the 19th century go to the South? They went to the industrial northeast or (as did my grandparents) to the midwest. The US in the 19th century was prosperous despite slavery in the south, not because of it.

Category: Economics, History |

Comments Off on Slavery Made the US Less Prosperous, Not More So

Apparently there is a new CBO report on the effect of a Federal minimum wage hike to $15. Before I get into the economic impacts, I want to observe that the $15 Federal minimum wage is a political smart bomb that hits mostly red states in much the same way as the reduced Federal tax deductions for SALT (state and local taxes) was a smart bomb that mostly hit blue states. From an equity standpoint it is insane to have the same minimum wage in rural Alabama as in San Francisco, but since its main negative employment effects will be in red states I think this may be a feature rather than a bug for Democrats.

Anyway, for years folks have made the argument that government-mandated minimum wages are necessary because of the power imbalance between employers and low-skill workers which allows employers to exercise monopsony power and keep wages below some theoretical market clearing price (which is a total laugh -- if you really believe this you can come to my company and try to hire for unskilled positions at the top of the economic cycle and see how much power we have). The progressive theory is that companies therefore earn excess profits due to this power.

But that is almost impossible. To actually profit from such power, a company would have to have a consumer monopoly and monopsony hiring power and those two are Venn diagrams that don't overlap much. As I wrote before (excerpt from a much longer piece)

Let’s consider a company paying minimum wage to most of its employees. At least at current minimum wage levels, minimum wage employees will likely be in low-skill positions, ones that require little beyond a high school education. Almost by definition, firms that depend on low-skill workers to deliver their product or service have difficulty establishing barriers to competition. One can’t be doing anything particularly tricky or hard to copy relying on workers with limited skills. As soon as one firm demonstrates there is money to be made using low-skill workers in a certain way, it is far too easy to copy that model. As a result, most businesses that hire low-skill workers will have had their margins competed down to the lowest tolerable level. Firms that rely mainly on low-skill workers almost all have single digit profit margins probably averaging around 5% of revenues (for comparison, last year Microsoft had a pre-tax net income margin of over 23%).

If there were some margin windfall to be obtained from labor market power that allowed a company to hire people for far less than their labor was worth to it, and thus earn well above this lowest tolerable margin, new companies would try to enter the market, probably by lowering prices to consumers using some of that labor premium. Eventually, even if the monopsony premium exists, it is given away to consumers in the form of lower prices. If the wholesale price of gasoline suddenly falls sharply, gasoline retailers don't get to earn a much higher margin, at least not for very long. Competition quickly causes the retailer's lowered costs to be passed on to consumers in the form of lower retail prices. The same goes for any lowering of labor costs due to monopsony power -- if such a windfall exists, it is quickly passed on to consumers.

As a result, the least likely response to increasing labor costs due to regulation is that such costs will be offset out of profits, because for most of these firms, profits have already been competed down to the minimum necessary to cover capital investment and the minimum returns to keep owners interested in the business.

I have not read the CBO report. Interestingly, apparently both Kevin Drum and CNBC have and they summarize the findings differently -- not just draw ideologically different conclusions but report the key data differently. I have not made any attempt to reconcile this (my guess is that Drum has picked the most optimistic case). But I will take this from Kevin Drum's version:

Total wages for workers would rise by $44 billion (accounting for both higher wages and increased joblessness). Income for business owners would fall $14 billion.

Consumers would pay higher prices amounting to a total of $39 billion. That’s an increase of about 0.3 percent.

You can see that the CBO obviously does not buy the progressive argument about excess corporate profits. 90% of the wage increase is paid for by consumers in the form of higher prices. My bet is that most of the business income loss is not margin compression as much as lost sales due to higher prices. Note also the inefficiency of the minimum wage even in these optimistic numbers -- consumers and businesses contribute $53 billion in value to increase wages by $44 billion. The rest is a net loss to the economy and my bet is that these numbers underestimate this loss.

The other problem with minimum wage increases as an anti-poverty program is that people are in the bottom 20 percentile of earnings mostly due to insufficient work hours, not due to wage rates. It turns out that increasing the wage rates of the poorest 20% to middle class levels yields $6,335 a year in gains for a person in the poorest 20% while increasing that same poor person's amount of work done to middle class levels yields $28,844 a year in gains (government data here). If you want to help poor people, economic growth and reducing barriers to hiring low-skill workers (combined with efficient transfer programs) is the way to go -- in this context the minimum wage increase can actually be counter-productive.

Last summer I had the cover story in Regulation Magazine titled, "How Labor Regulation Harms Unskilled Workers." I fear we are heading to a European model of very high minimum costs of employing anyone, which tends to result in a two-tier system of well-paying jobs for skilled and educated employees and lifetime government relief for the unskilled and under-educated.

Category: Economics |

Comments Off on Minimum Wage Increases Are Mostly Paid for by Consumers